I. INTRODUCTION

For decades, the Federal Reserve has released public statements to reflect the economic situation as well as to communicate potential policy trends (Doh, Kim & Yang, 2021). The Federal Open Market Commitment (FOMC) exercise “forward guidance” in their statements, including both qualitative and quantitative information (Doh, Kim & Yang, 2021). There are three types of FOMC documents—statements, minutes, and transcripts. These documents basically differ in length and timing¹. In addition to these, there are alternative statements that incorporate extra information and further implications.

On most occasions, the FOMC statements will explicitly set the target in quantitative terms. However, the qualitative description of the statements is of equal importance. Different from numeric data, it is difficult to reveal effects of the quantitative information in a direct manner. However, we can measure the tone of the documents with the assistance of current text analysis and machine learning techniques.

This paper hereby intended to address two questions. By exanimating the text-based documents, we would like to study how the content of the FOMC documents evolved over time. The other essential exploration would be how does the FOMC documents related market responses, which can be reflected on the US Treasury Bond rate with different maturity.

II. LITERATURE REVIEW

Application of Text Analysis in Public Statements

Scholars have valued more and more of textual data because of the limited availability of quantitative data and manipulation of the numbers (Lucas, 2015). Exploring public statements has become an increasing popular topic. While some are interested in the official documents released by international organizations, such as United Nations and World Bank (Mansell, 2014), others have focused on studying the public statements at national level, such as the US Federal Reserve (Shapiro & Wilson, 2021) and Reserve Bank of India (Pandey & Shettigar, 2021), and so on.

Existing studies applied text analysis either to explore the text or to test the relationships among the documents and external factors. Cannon (2015) has employed text mining to study FOMC transcripts. By closely investigating the information in the documents, Cannon (2015) explored the general trend (such as length and frequency, etc.) of those publicly available files, and the tones revealed by the dictionaries with different focuses. Mazis and Tsekrekos (2017) adopted Latent Semantic Analysis (LSA) to identify topics. Siklos (2020) used a mix method including Wordscores and DICTION to capture the essence of FOMC minutes, revealing that the document content is closely linked with GDP changes and Fed Fund Rate Changes. Edison and Carcel (2021) analyzed FOMC transcripts using Latent Dirichlet Allocation (LDA) and the Stata command Idagibbs in particular. They concluded that topics of the documents evolved over time and special events, such as global financial crisis would affect the topics covered in the statements (Edison and Carcel, 2021).

Some existing papers are also curious about the relationship between equity market and FOMC announcements (Zebedee, 2008; Farka, 2011; Farka & Fleissig, 2012; Bailey, 2017; Cieslak & Vissing, 2019). But former studies were based more on exploiting the qualitative information in the statements. However, recent research concentrates more on utilizing the qualitative information or a mixed approach.

Huang and Kuan (2021), apart from investigating closely into the content of FOMC document, studied its relationship with economic development by virtue of text mining. In particular, the Bayesian approach was used to construct the sentiment indicators for each document. Like the findings in Edison and Carcel (2021), Huang and Kuan (2021) also found the changing feature. In addition, they realized the predictive power of such public statements. Employing the NLP, Doh, Kim and Yang (2021) studied FOMC statements in a 10-year period and found that qualitative message conveyed are as important as quantitative indicators. Moreover, they found that different interpretation of the same events matters and could lead to the fluctuation of the overall tone of the documents that pass to the market (Doh, Kim & Yang, 2021).

Shapiro and Wilson (2021) adopted sentiment analysis to estimate the implicit inflation preference of FOMC statements and the underlying rationales for FOMC’s decisions. They found that FOMC placed great emphasis on the status quo of stock market returns (Shapiro and Wilson, 2021). Baerg and Lowe (2020) has combined both topic modelling and scaling methods to estimate central bank preferences. They contributed by using FOMC members’ preference to compute the ideal-point estimates. Interestingly, they uncovered that effect of voting behaviors may sometimes appear to be inaccurate while text-based analysis of the speeches demonstrates greater variation.

Rationales for Financial Market Reaction

Existing literature has discussed various themes of market responses. This part aim to present some of the featured and essential ones. Among then, the first thread is factor analysis on the yield of US treasury bonds. Goeij and Marquering (2006) found that employment data and Producer Price Index (PPI) affect the medium- and long-term bond volatility. Huang and Lu (2008) used the principal component analysis to extract real-economic factors and monetary factors from macro-level economic data. They found that macro factors have a significant effect on the volatility of bond returns. Real-economic factors, including PPI and unemployment rate, can affect the volatility across all maturities. By comparison, monetary factors, such as the Federal Funds Rate (FFR) and Money Stock (M2), are associated significantly with the return volatility of short-term bonds but weakly with the return volatility of medium-term bonds.

Ivo and Evert (2010) indicated that there is a clear causal relationship between monetary policy uncertainty (but cannot be quantified) and treasury bond. Among various kinds, the dispersion-based uncertainty about the future course of monetary policy being the most critical determinant. As such, the real-economic variables can explain a large fraction of the bond yields across all maturities although there is still certain level of controversy among different scholars regarding the path and difference in terms.

The other thread indicates that information published by institutions has impacts macro-economically. Pierluigi et al. (2001) found that public news could explain a substantial fraction of the price volatility of 3-month term, 1-year term, 5-year term, and 30-year term bonds. The explanatory power varied markedly according to the maturity of bonds.

Then, Anderson et al. (2003) studied that positive and negative news have asymmetrical impacts on the macroeconomy. Their empirical evidence showed that some institutions could seriously impact the foreign exchange market or the economic environment after publishing bear news. By contrast, cheerful information is difficult to impact positively. Campbell et al. (2012) figured out that the meeting content of FOMC plays the role of forward guidance, which has macro-level effects on financial markets. Meanwhile, the sentiment content of the FOMC could be influenced by the economic context.

Scott and Victor (2018) pointed out that positive and negative words proportion of each Federal Reserve chair are different significantly across various chairman, including Greenspan, Bernanke, and Yellen, and speeches are also impacted considerably by macroeconomic factors, such as Gross Domestic Product (GDP) and Consumer Price Index (CPI). This finding informs us that the chairman dummy variable might be a good control variable in the regression model.

Although text analysis is now emerging in various fields including both the public and private sectors, they oftentimes appear to be too narrowly focused. The following study will make efforts in uncovering the evolution of content in two of major types of FOMC documents, proving a comprehensive picture of how the content derived from the same meeting differs and how the content of different meeting within one single type changes over time. Moreover, the information embedded in the documents can be an excellent source for predicting future trend more accurately. Quantifying those hidden effect in relation to market response can help people make preparation if any window exists.

III. METHODOLOGY, DATA AND MEASUREMENT

We obtained texts from the website of US Fed Reserve (https://www.federalreserve.gov) and pretest with the shortest and most timely versions—the FOMC statement. With web crawling, 132 files were collected. The first task was to find out patterns demonstrated by the collection of files, such as word frequency (count, frequency, and tf-idf) and the sentiment embedded in different file.

In addition to uncovering the evolution of the content as well as some of its underlying implications, we also explore relationship between public communication and the yield of US Treasury Bonds. As previous studies (Goeij and Marquering, 2006; Huang and Lu, 2008; Ivo and Evert, 2010; Anderson et al., 2013) pointed out that bond yields are associated with macroeconomic conditions, such as GDP, inflation, and employment data. In this paper, we used the yields of 13 weeks, 2-year, 5-year, 10-year T bonds as dependent variables, whereas sentiment scores (including specific scores such as uncertainty scores and overall scores) and several typic indicators representing the macroeconomic conditions are set as the independent variables. Before performing the regression analysis, we came up with several hypothesis:

: All sentiment scores are strongly linked with the yield of US Treasury Bonds with different maturities, including both the value and the volatility in given period.

: The sentiment scores affect the yields² differently (whereas some may even have no significant impacts), but their impacts on value and volatility are not separatable³.

: The sentiment scores affect the yields differently (whereas some may even have no significant impacts), but their impacts on value and volatility are separatable.

: The sentiment scores have no impacts on the returns of the US treasury Bonds.

In the event of any relationship identified (as in , , ), we will further expand the existing research to seek more accurate relationship (if any) between files and yield.

IV. RESULTS AND ANALYSIS

Text Data Mining: Pattern, Implication and Evolution

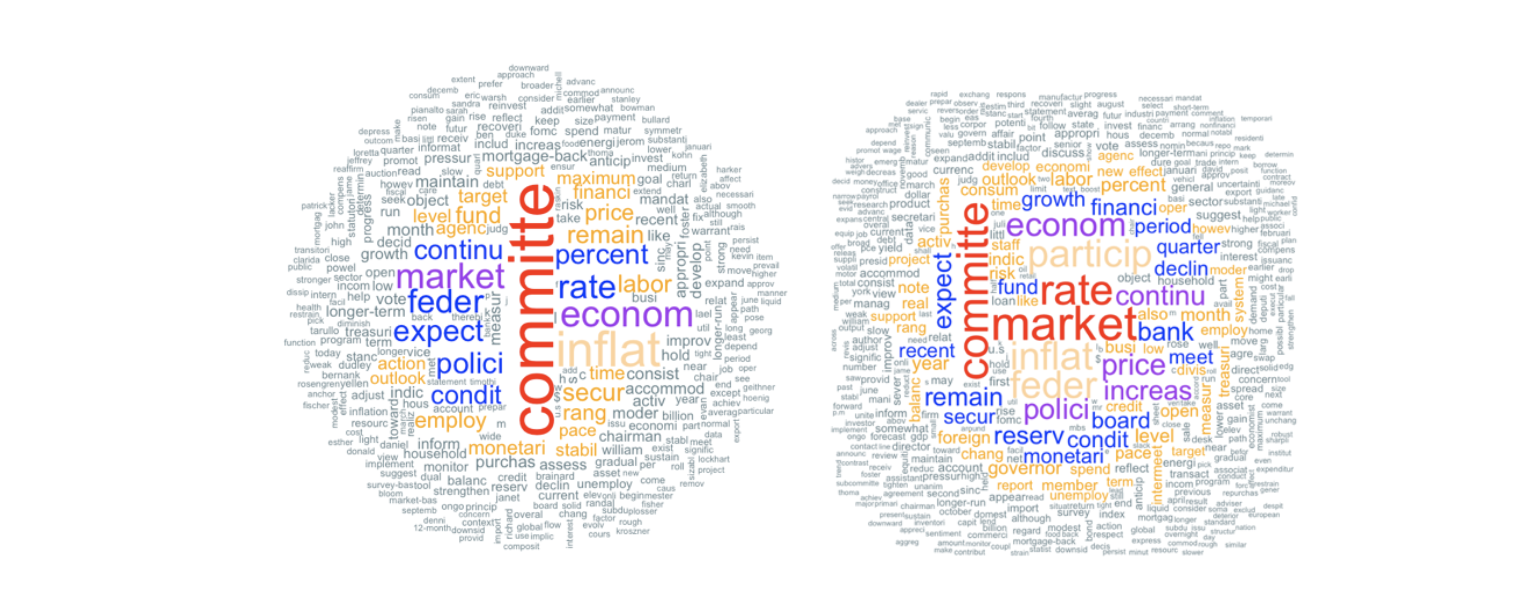

The word cloud generated from the two kinds of FOMC files showed similar results, with the key words “committee” “market” “economy” “rate” “expect” all emerged in them as the most frequent. In terms of word count, we can find that the word count in FOMC statements showed an increasing trend from the beginning of the selected period to September 2015 (Figure 3). After that, the wordcount demonstrated a decreasing trend and bottomed out in March 2020. The pattern is difficult to capture. In the case of FOMC minutes, the overall trend is increasing with peaks occurred regularly. After careful observation and some calculation, we found that wordcount peaked in the first FOMC minutes each year (more than 60% of the peaks).

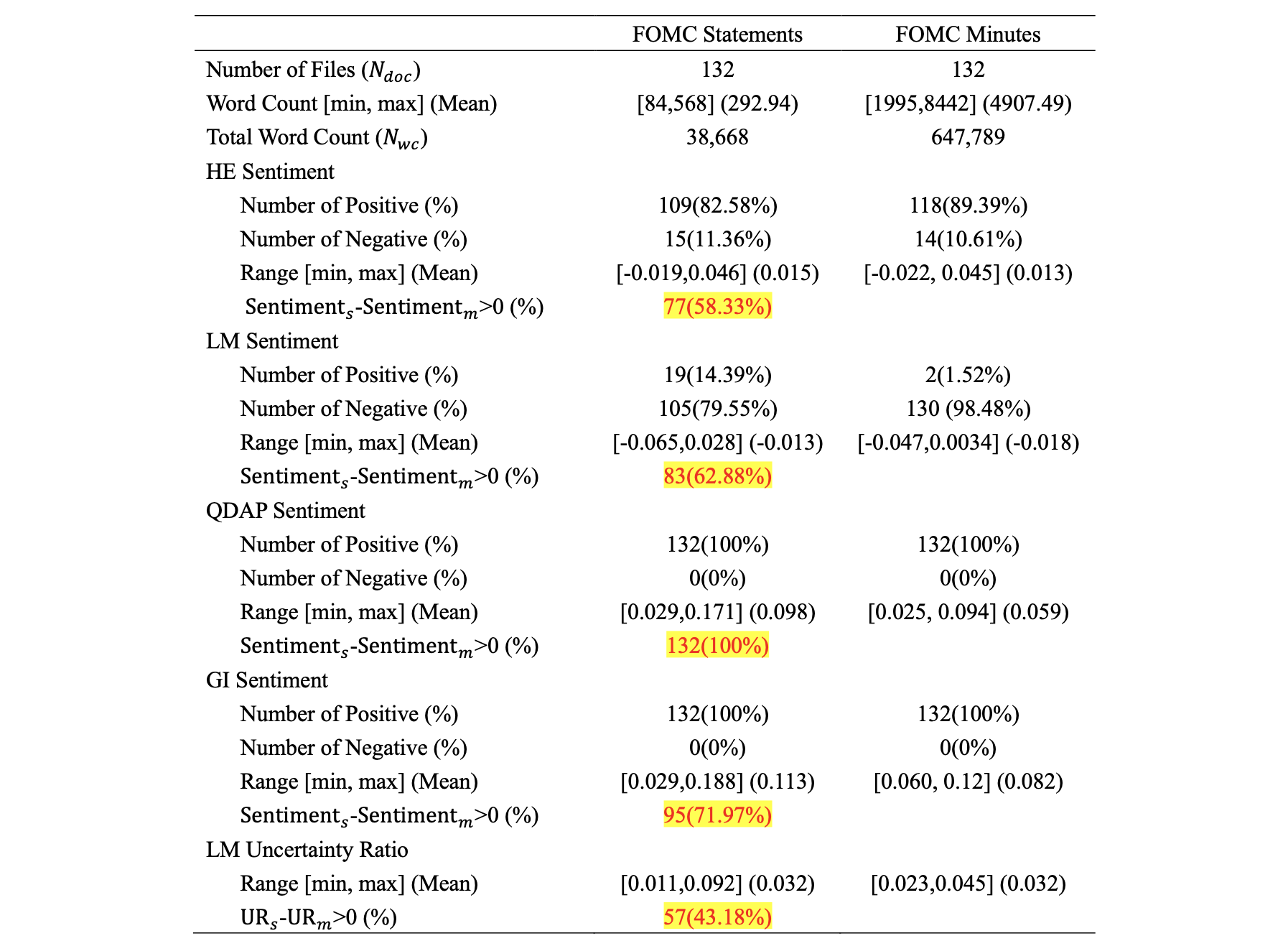

We examined the overall sentiment score of 132 FOMC Statements and Minutes using the SentimentAnalysis package in R, which included several professional dictionaries such as the finance-specific dictionaries (HE and LM) by Henry (2008) and Loughran & McDonald (2011) as well as the Harvard-IV dictionary used in the General Inquirer software (GI). Apart from the overall sentiment score, the LM dictionary also generate an Uncertainty Ratio that is separable from traditional measurements such as positive and negative scores.

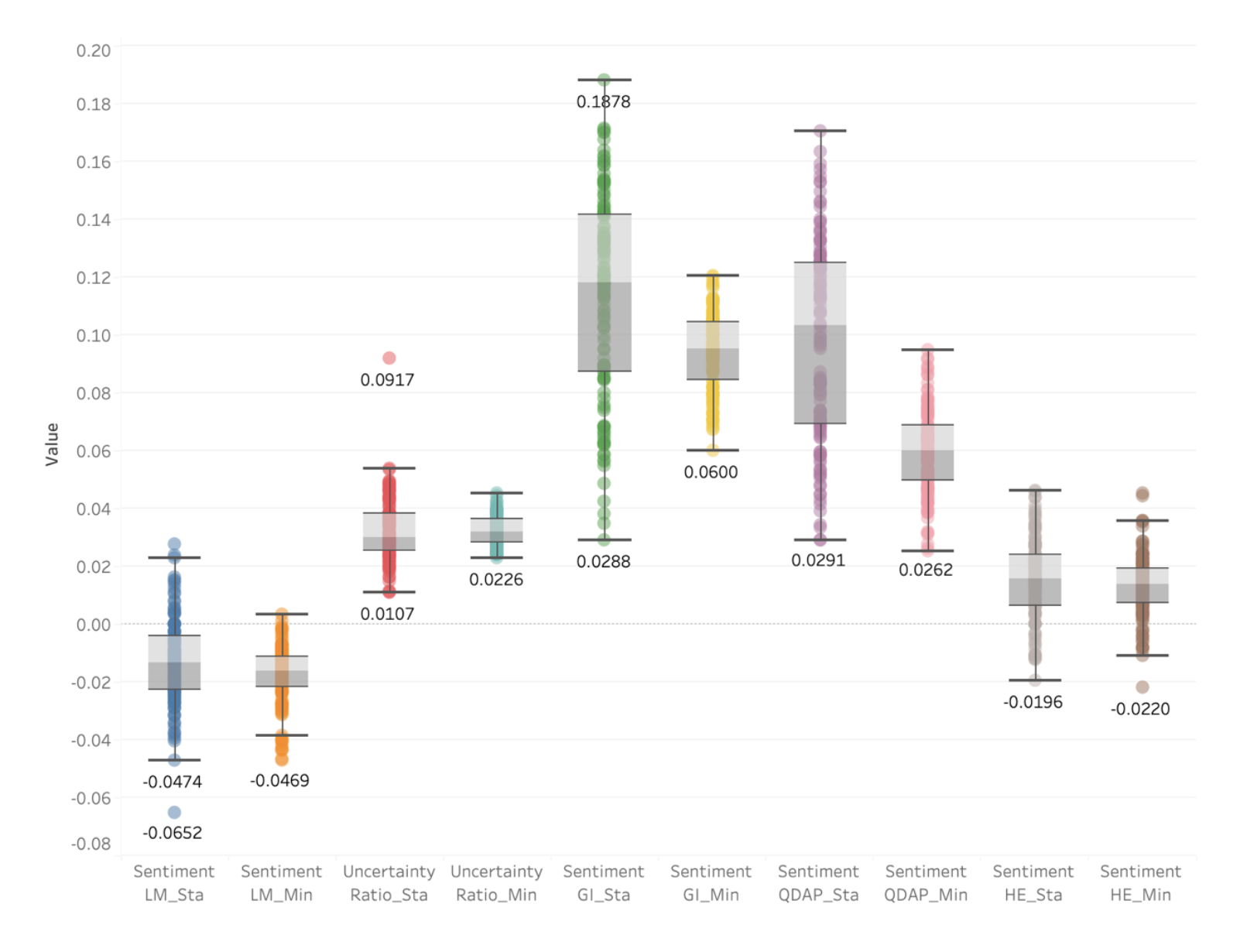

The results showed no evident pattern of the proportion of positive sentiment and negative sentiment at the general level across all those dictionaries. However, the means are always higher in FOMC statements than those in the minutes. When we considered the differences of the sentiment, it is found that scores of statements are always higher than those in the minutes. The conclusion can be drawn from highlighted parts in table 1. The uncertainty ratio, however, is lower in the statements. To learn the distribution of the sentiment in a more straightforward manner, we attached the box plots as below.

In addition to the above findings, we can conclude that the sentiment ranges (including uncertainty ratio) of the Statements are wider than those of the minutes. After all these have been explored, we considered time effect and difference in pair at individual levels.

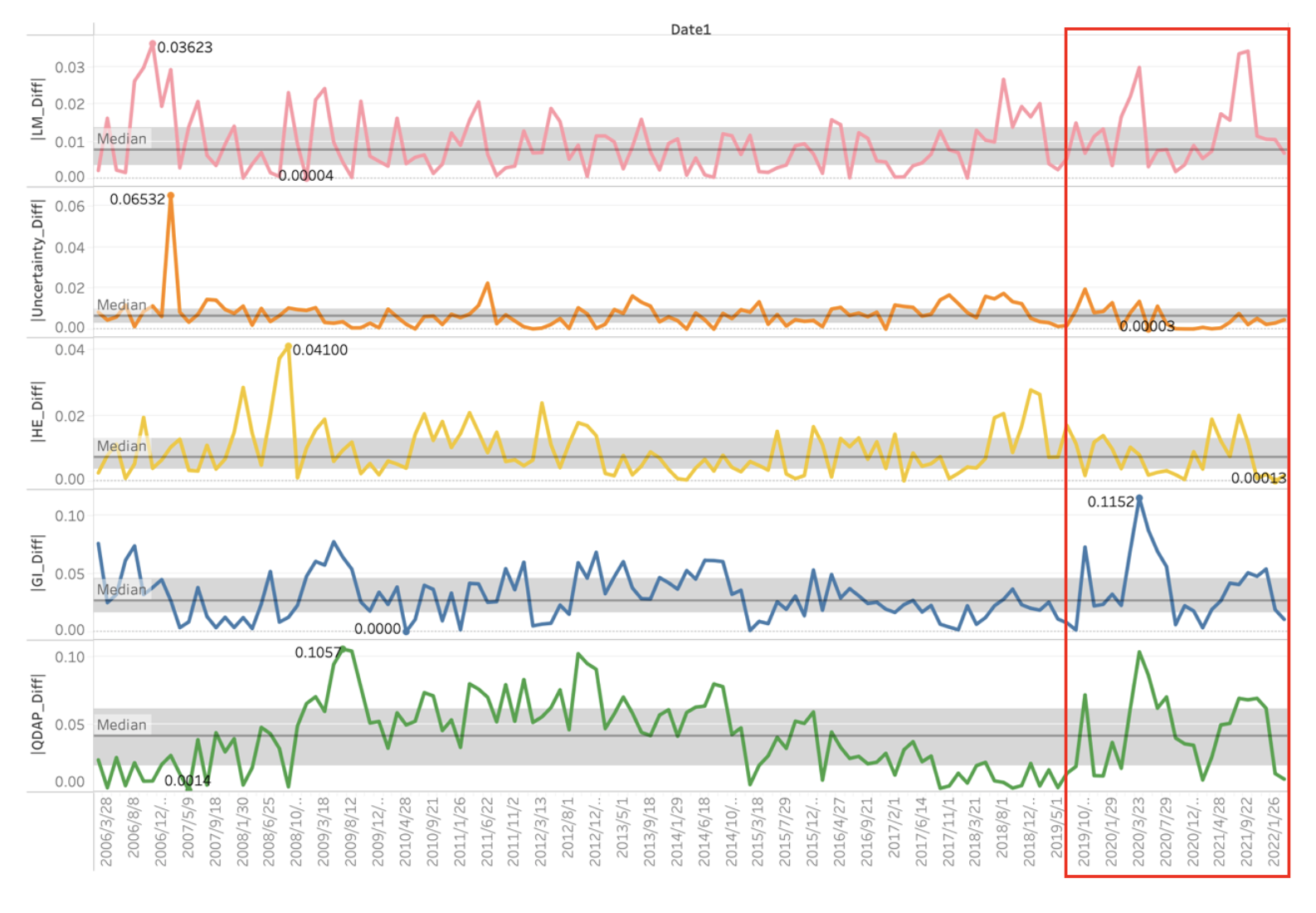

We use the absolute value to represent the differences of sentiments between two files for each same meeting. It is found that the differences of the uncertainty ratio are rather stable across time. By contrast, the overall sentiments fluctuated over time. But a closer observation indicates that as time evolves, differences narrowed (see the outliners out of the 1/4–3/4 band) except for the period from the end of 2019 to 2022.

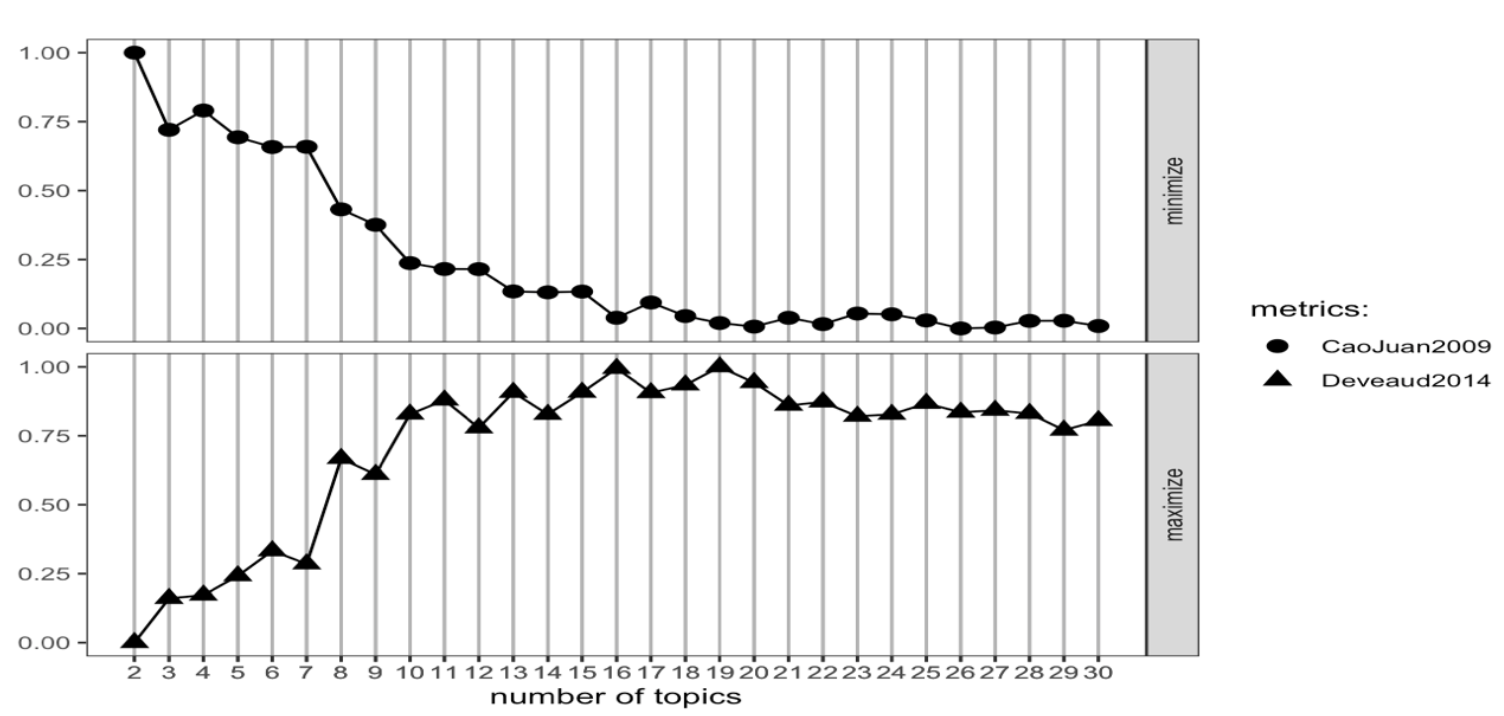

We also explored the changes of content of the statements and minutes by the assistance of LDA topic modeling. We compared the changes within each type. The topic numbers was decided by ldatuning::FindTopicsNumber function in a package named ldatuning. We plot the model fit using two metrics—Caojuan2009 and Deveaud2014. Tradeoff between the two metrics determines the best fit. In our testing, when topic number , the best coherence achieved in the FOMC statements (see below). And for the minutes, returns the best cohesive outcomes for topics.

There are certain patterns of the topic distribution over time in two types of FOMC files. At the very beginning, the content of the statements was dominated by one single topic. Later on, the previous topics shifted to another one. Rarely the topics overlapped expect for a period from 2013 to 2018 when several main topics coexisted.

In terms of the FOMC minutes, the shift of topics occurred more gently, with relatively long time for the transition to emerge, meaning that the overlapped topics were common. Another interesting pattern for the minutes is that the occurrence of some being cyclical. Potential reasons for the above findings are that FOMC statements are in general short, and such conciseness indicates that each time only limited information will be conveyed. However, the minutes are long, and advantage in length enable it to incorporate more information. In addition to this, the minutes might inherently emphasize the transition, by which the board members can recall the last meeting and make vision for the future.

Regression: A Basic Exploration with OLS Model

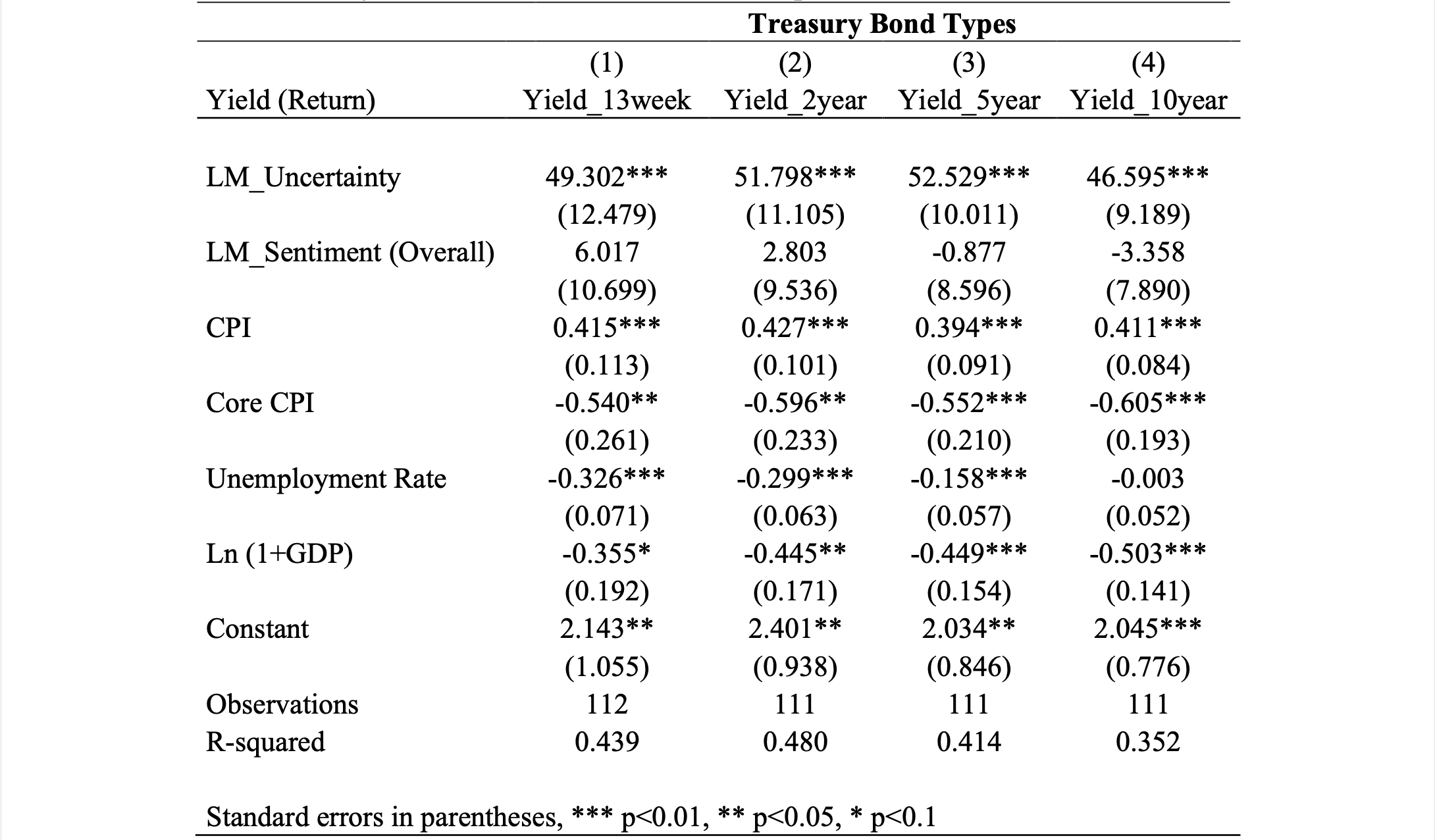

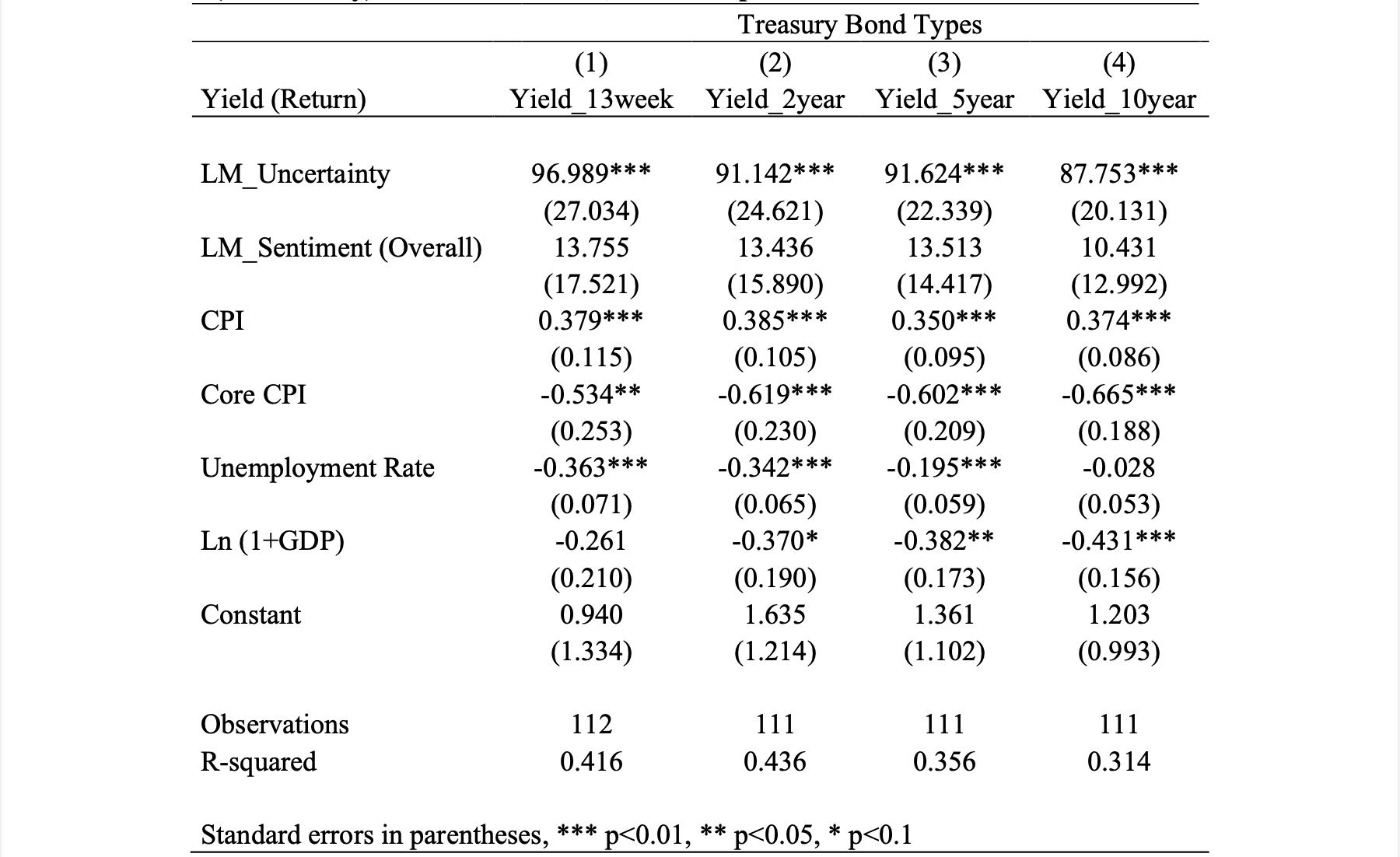

In this subsection, we would like to explore the relationship among the return of various US Treasury Bonds along with sentiments (LM selected) and macroeconomic factors. Table 2 shows four multiple regression models that take sentiment scores (and the LM uncertainty ratio) of Statements and yields of different-maturity bonds, including 13-week bonds, 2-year bonds, 5-year bonds, and 10-year bonds, as the outcome variables. At the same time, it also shows estimated coefficients of all explanatory variables using the ordinary least squares (OLS) method. Table 3 shows the results using same variables based on a different type of FOMC documents, Minutes.

In general, the mean of eight regression models’ R squared is about 0.4, indicating that our models have a qualified ability to explain the value of the yields, nearly 40 percent. Meanwhile, impacts of macroeconomic indicators on bond yields are consistent with our expectations. For example, there is a positive relationship between bond yields and CPI that could be regarded as a measurement of inflation. If inflation becomes severe, the return of bonds would be diluted. Investors have to sell their bonds to avoid further loss, which causes bond yields to increase. The results also presented a negative relationship between unemployment rate and bond yields. The Federal Reserve is more likely to lower interest rates to stimulate the economy when unemployment rate rises. The consequence for this is the decrease of yields, and the investors will turn to more active investments.

More importantly, we have obtained some interesting findings by the results revealed by the two tables, and they are listed as follows:

Firstly, the uncertainty ratio (also part of the sentiment in LM sentiment) of both types of documents are statistically significant in relation to the bond yields. If the uncertainty sentiment is high, bond market investors may feel so dizzy that they concerned more of the potential directions. Thus, they are more willing to sell the unmatured bonds on the secondary markets and reduce their positions on the defensive. A lot of sell bills finally caused the prices of bonds to decrease and the yields to increase. Moreover, the average coefficient of the uncertainty ratio in Table 2 is nearly twice as much as that in Table 1, an outcome that might result from difference in level of detail between the two types.

Secondly, overall sentiment score of both Statements and Minutes has no statistically significant impact on the yields of bonds. This might be the consequence of only minor discrepancy between the investors’ expectation of sentiment and the sentiment revealed.

Thirdly, the impacts of CPI on bond yields are always statistically significant, and the coefficient does not vary obviously with maturities. However, the effects on the natural log of GDP become more and more significant as the maturity of the bonds extend. On Table 3, such pattern is more evident. Model (1) shows that the natural log of GDP has no significant impact on the yield of a 13-week bond, while Model (4) shows that it has significant effects on the yield of a 10-year bond at a 1% significance level. At the same time, the magnitude of the impact becomes larger as the terms being longer, implying that long-term bonds are more affected by actual economic products.

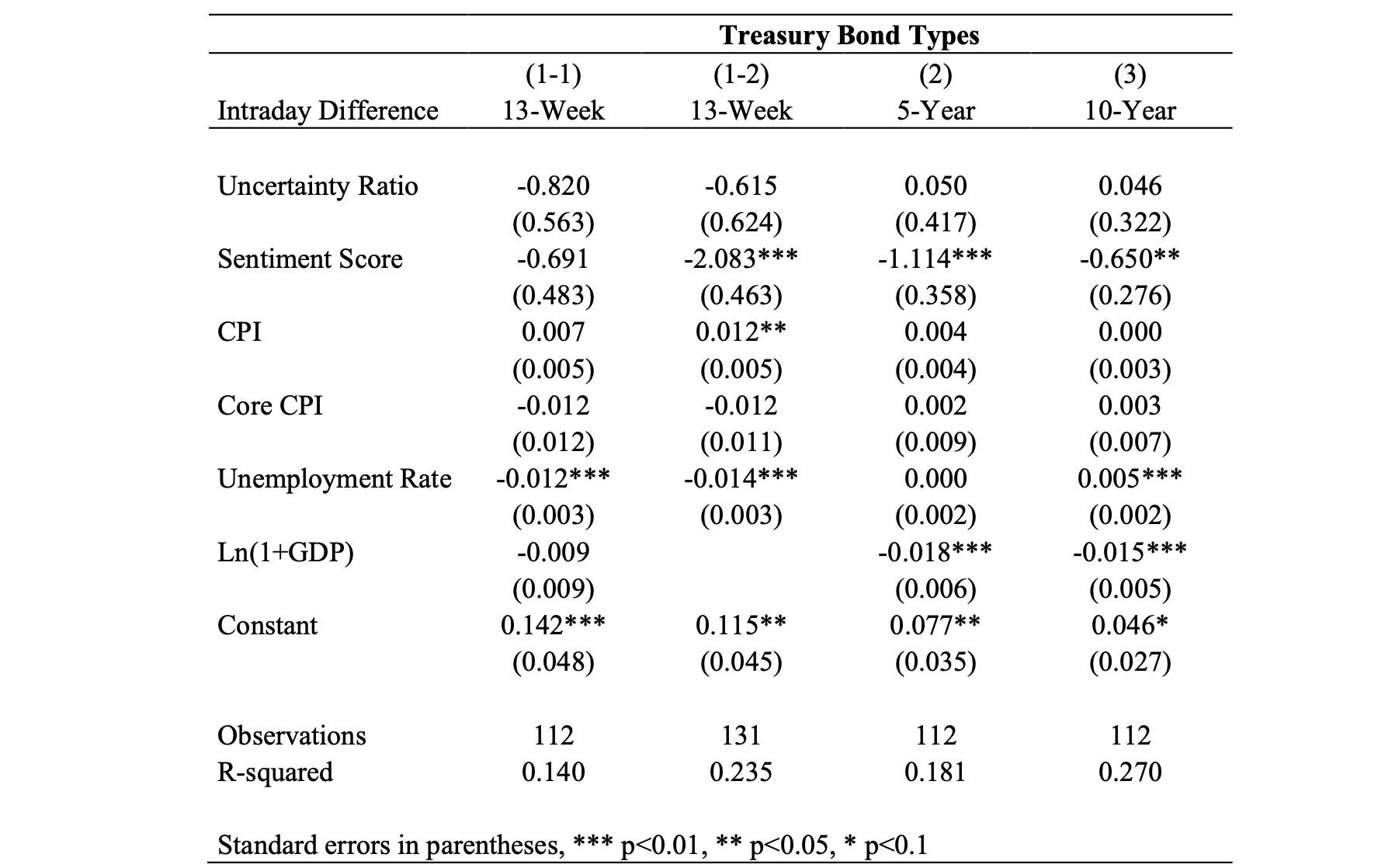

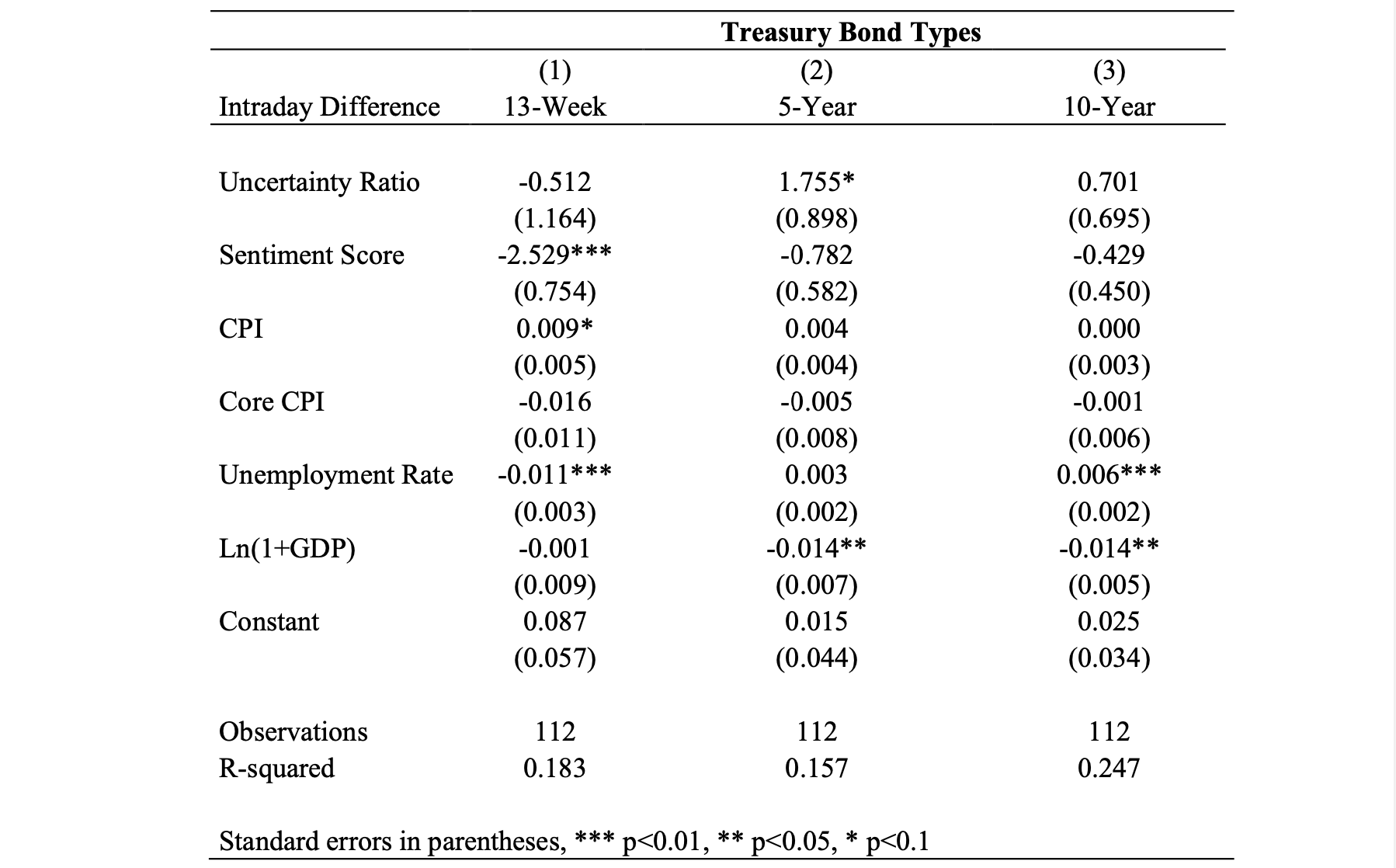

We further explored the potential linkage among various factors by considering the intra-day difference of the yields. Table 4 shows four multiple regression models that take sentiment scores of Statements and intraday yield volatility of different-maturity bonds, including 13-week bonds, 5-year bonds, and 10-year bonds as outcome variables⁴. Table 5, in a similar manner, shows three multiple regression models based on the sentiment scores of Minutes and intraday yield volatility and related estimations using the OLS method. We also obtained some interesting and valuable findings by analyzing the outcomes of the two tables. The most critical finding in Table 4 is that the sentiment score of Statements has a statistically significant relationship with the intraday yield volatility of different-maturity bond.

Moreover, we can see a negative relationship between the sentiment score and yield volatility, and the coefficients of the sentiment score on yield volatility decrease as term increased. As being more liquid and less risky (Smart asset, 2019), the short-term bonds are suitable for speculation, meaning that investors make profits by looking for price gaps frequently. However, speculators seek to earn abnormally high returns from bets that can go one way or another (Investpedia, 2022), and thus speculative trading is more susceptible to emotion. Nevertheless, due to the time lag, the sentiment of minutes (may subject to adjustment) might not show relationship in a retrospective way.

Apart from the above findings, we also find that inflation indicators and the uncertainty ratio generally have no significant impact on the intraday yield volatility of bonds with various maturities. In terms of the uncertainty ratio, investors may not have enough time to analyze the uncertain part of files in trading time. In terms of inflation indicators, the range of monthly changes in the indicator can be expected efficiently by institutional investors, so the intraday trading of bonds will not be impacted.

Overall, when we take the absolute closed yields as the outcome variable, and consider some essential economic indicators, the uncertainty ratio of FOMC files has statically significant implication, which may stem from investors’ knee-jerk defensive behaviors. Generally, increasing one percent of the uncertainty ratio of Statement, the closed yields of different-maturity bonds rise 50 bps in mean. Likewise, by raising one percent of the uncertainty ratio of Minute, the closed yields of different-maturity bonds increase 90 bps on average. On the other hand, the sentiment score of files has a significant impact on the volatility statistically, and its magnitude decreases with longer maturities.

V. DISCUSSION, CONCLUSION, AND IMPLICATION

Generally speaking, the Statements and Minutes did not differ greatly in content. But the wordcount of the first Minutes generally be the maximum of the year. Adjustment of sentiment between the two types might gradually narrow as time evolves. In terms of topic focus, the Statements demonstrated a shift pattern whereas the Minutes focused more on the smooth transition.

We found that LM Uncertainty Ratio is positively related to yields of the treasury bonds with different maturities. All our testes reaffirm that they are statistically significant. Although there is no direct trend of impact intensity regarding the maturity, the middle-term treasury bonds are affected the most. And while the overall sentiment does not show significant linkage with the close value of the bonds as people normally expected, they affect the rate in another way, that is the volatility of rate in selected days.

Due to the absence of more specific and detailed information of intraday data (e.g, how the rate changed in minutes and hours), it is hard for us to pinpoint the most profitable window for intraday investement. Neverthless, the previous conclusions have offered some hints regarding the close yields and the intraday difference of the rates. Combined togetehr, they can still assit to seek some investemnt chances that are likely to generate favorable outcome. While the closed value is strongly linked with uncertainty ratio, the overall sentiment help forecast how great the changes will occur with the direction (+/-).

From another perspective, policymakers should pay special attention to the way they communicate with the public, our paper and previous studies all pointed to one direction, that “public communication can affect financial market conditions” (Hearit, 2018; Eberly et al, 2019).

VI. LIMITATIONS AND FURTHER STUDIES

Although our study is based on the strategic combination of qualitative and quantitative methods, there are some limitations that we would like to communicate with our readers.

- • (1) The selection of outcome variables might not be the complete representation of the real circumstance. While the release of the FOMC documents can be anytime of the day, the price can sometimes be closed before the announcement made. We did not take this effect in our studies, which might lead to some measurement errors.

- • (2) The availability of other dependent variables constrained the accuracy of our studies. Most of the macroeconomic indicators are published on the quarterly basis. As such, the time scale might not be compatible with our research. We partially reduce errors brought by the inconsistency of time by considering chronological orders to match with real practice. For example, for the statements released in January, we selected the Q4 data last year to present the economic conditions.

- • (3) Given that the Treasury Bonds are more stable in its returns, the translation of the capital gains depends largely on the scale of investment. For such reasons, the study is more applicable for investors with large-scale investments, such as institutions.

There are several improvements and areas that can be considered for further research. For example, more accurate research can be realized by obtaining the exact release time of the FOMC statements. Depending on the time, the outcome variables can be changed as the rate in a more specific and narrowed time scope after the publish of the statements (e.g., 3 minutes, 5 minutes, 2 hours, etc...). Another potential area for further studies is studying the relationship between the sentiments and the stock market performance.